2024 Reports 5 to 7 of the Auditor General of Canada to the Parliament of CanadaReport 6—Sustainable Development Technology Canada

Independent Auditor’s Report

Table of Contents

- Introduction

- Findings and Recommendations

- Sustainable Development Technology Canada did not establish clear assessment guidance to determine eligibility of projects

- The foundation poorly managed conflicts of interest

- The board of directors failed to oversee the foundation’s compliance with key legal requirements

- The department did not sufficiently assess whether the foundation complied with the contribution agreements

- Conclusion

- About the Audit

- Recommendations and Responses

- Exhibits:

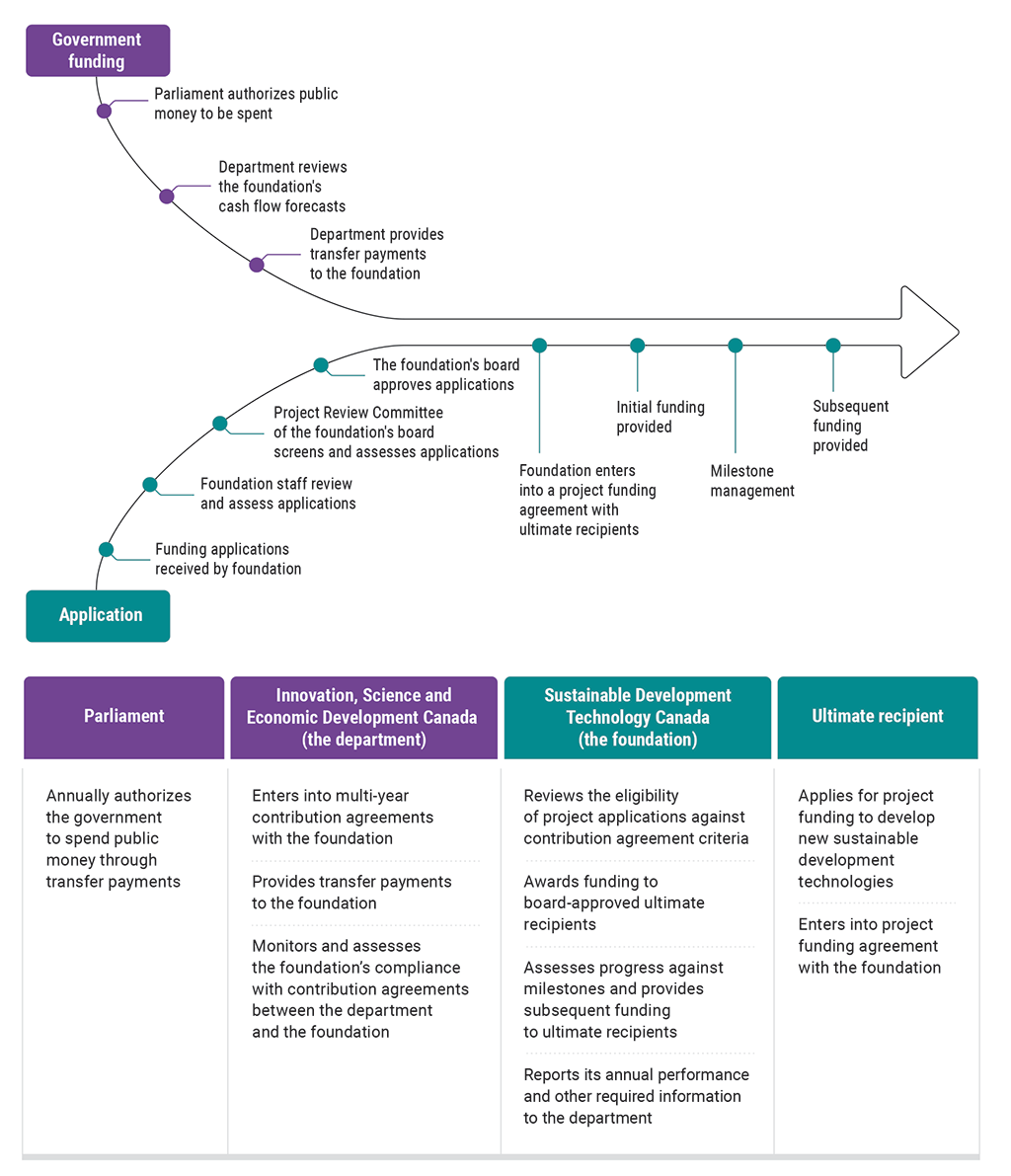

- Exhibit 6.1—Funding process for most applications to the Sustainable Development Technology Fund

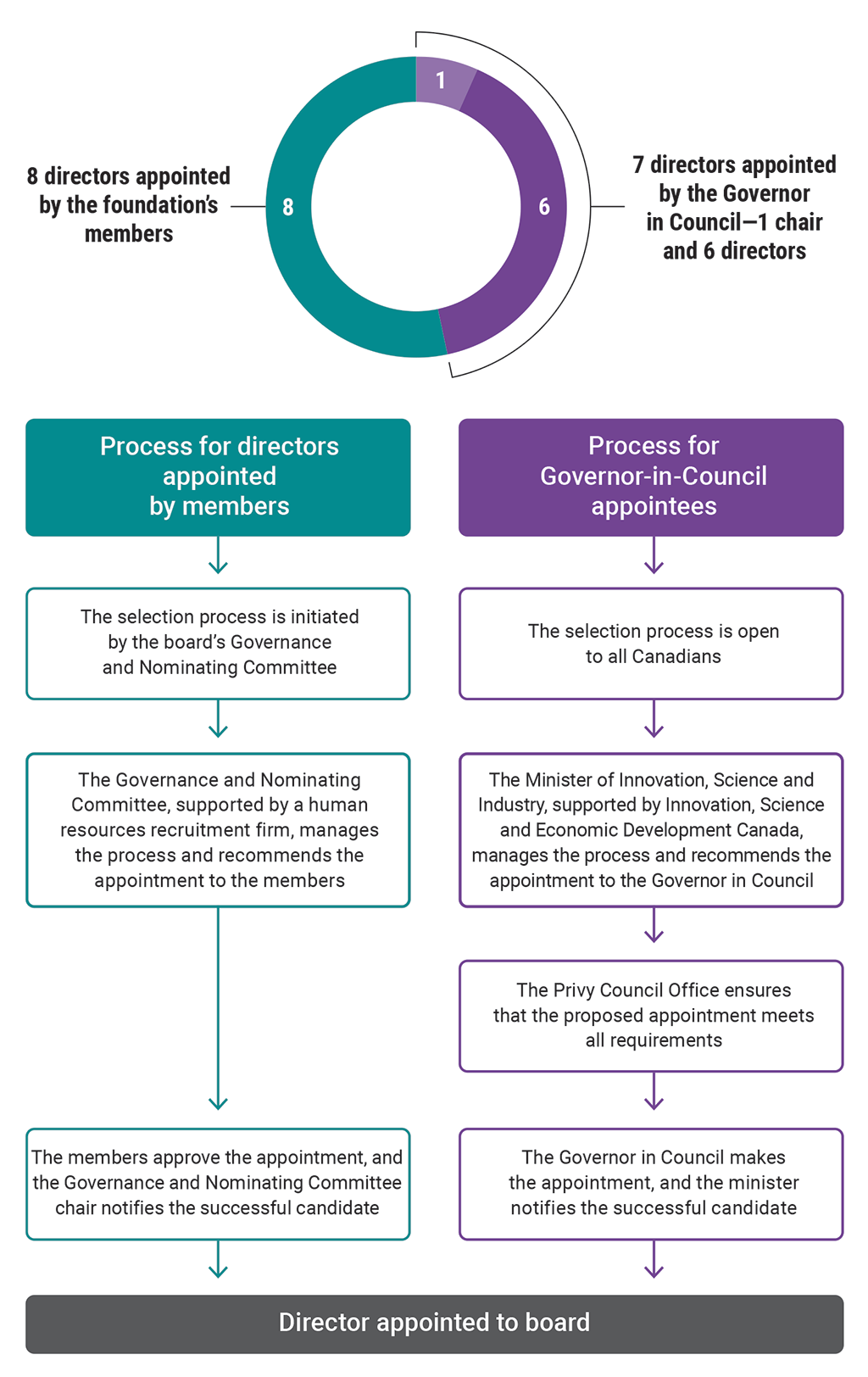

- Exhibit 6.2—Process to appoint directors to the board of Sustainable Development Technology Canada (the foundation)

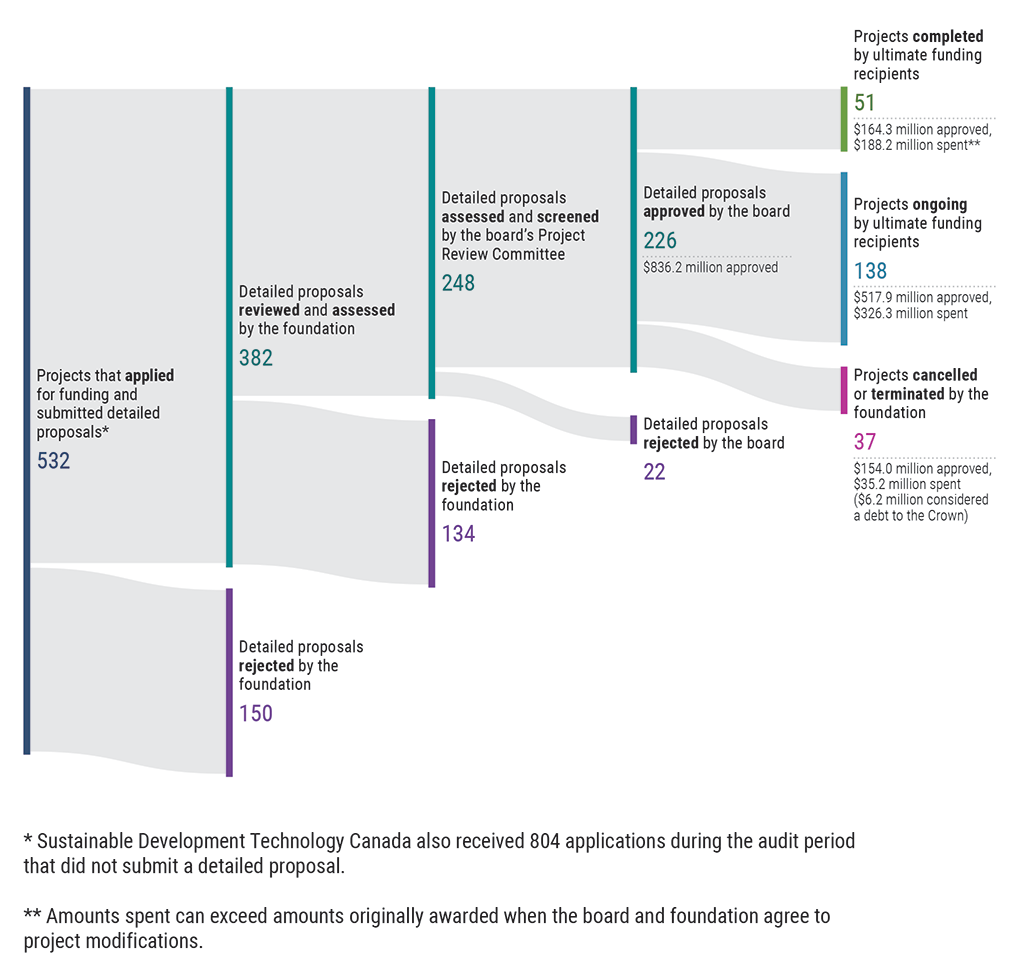

- Exhibit 6.3—Results of applications to the Start‑up, Scale‑up, and Ecosystem streams of Sustainable Development Technology Canada (the foundation), 1 March 2017 to 31 December 2023

- Exhibit 6.4—Records showed that conflict‑of‑interest policies were not followed when nearly $76 million of funding was approved during our audit period

Introduction

6.1 Sustainable Development Technology Canada (legally, the Canada Foundation for Sustainable Development Technology) is a federally funded arm’s‑length foundation created in 2001 and operated as a not‑for‑profit corporation. Its mandate is to award funding for eligible projects carried on primarily in Canada to develop and demonstrate new technologies related to climate change, clean air, clean water, and clean soil in order to make progress toward sustainable development.

6.2 Since its inception, the foundation has entered into contribution agreements with the Crown, most recently, the Minister of Innovation, Science and Industry, to manage the Sustainable Development Technology Fund. According to these contribution agreements, the fund’s goal is to advance clean technology innovation in Canada, specifically by funding and supporting technology projects at the pre‑commercial development and demonstration stages (Exhibit 6.1).

Exhibit 6.1—Funding process for most applications to the Sustainable Development Technology Fund

Source: Based on the contribution agreements between Innovation, Science and Economic Development Canada and Sustainable Development Technology Canada

Exhibit 6.1—text version

This flow chart shows how the federal government funds most applications to the Sustainable Development Technology Fund.

Government funding

Government funding involves Parliament and Innovation, Science and Economic Development Canada.

Parliament annually authorizes the government to spend public money through transfer payments.

Innovation, Science and Economic Development Canada enters into multi-year contribution agreements with the foundation Sustainable Development Technology Canada, provides transfer payments to the foundation, and monitors and assesses the foundation’s compliance with contribution agreements between the department and the foundation.

The government funding process to provide contributions to the foundation is as follows:

- Parliament authorizes public money to be spent.

- The department reviews the foundation's cash flow forecasts.

- The department provides transfer payments to the foundation.

Application

The application process involves Sustainable Development Technology Canada and ultimate recipients.

The foundation reviews the eligibility of project applications against contribution agreement criteria, awards funding to board-approved ultimate recipients, assesses progress against milestones and provides subsequent funding to ultimate recipients, and reports its annual performance and other required information to the department.

An ultimate recipient applies for project funding to develop new sustainable development technologies and enters into a project funding agreement with the foundation.

The process for most applications to the foundation is as follows:

- Funding applications are received by the foundation.

- Foundation staff review and assess applications.

- The Project Review Committee of the foundation's board screens and assesses applications.

- The foundation's board approves applications.

- The foundation enters into a project funding agreement with ultimate recipients.

- Initial funding is provided.

- Milestones are managed.

- Subsequent funding is provided.

6.3 In February 2023, Innovation, Science and Economic Development Canada received allegations of financial mismanagement and poor human resource management practices at the foundation. In March 2023, the department hired an external consultant to conduct a fact‑finding exercise to determine whether there were sufficient facts to support a subsequent investigation. The report, completed in September 2023, identified inconsistencies and opportunities to improve practices related to governance, conflict of interest, compliance with the contribution agreements, and human resources. In November 2023, the department announced that a law firm would be hired to review alleged breaches of labour and employment practices and policies. This review was ongoing at the time that we completed our audit.

6.4 In November 2023, the Office of the Auditor General of Canada decided to conduct an audit to support parliamentarians in their oversight of government activities and the stewardship of public funds.

6.5 Sustainable Development Technology Canada. The foundation was established under the Canada Foundation for Sustainable Development Technology Act. It is governed by a board of directors that is composed of 15 voting directors. Directors are appointed in 1 of 2 ways (Exhibit 6.2). The Governor in CouncilDefinition 1 appoints 7 directors, 1 of whom is appointed as the board chair. Once appointed, directors have a fiduciary responsibility to the foundation. The foundation’s members (see paragraph 6.7) appoint the remaining 8 directors. The foundation’s Chief Executive Officer (CEO) also sits on the board and all its committees as a non‑voting member.

Exhibit 6.2—Process to appoint directors to the board of Sustainable Development Technology Canada (the foundation)

Source: Sustainable Development Technology Canada and the federal government website for Governor‑in‑Council appointments

Exhibit 6.2—text version

This flow chart shows the 2 ways that directors can be appointed to the board of the foundation Sustainable Development Technology Canada.

Eight directors are appointed by the foundation’s members. Seven directors are appointed by the Governor in Council—1 chair and 6 directors.

Process for directors appointed by members

- The selection process is initiated by the board’s Governance and Nominating Committee.

- The Governance and Nominating Committee, supported by a human resources recruitment firm, manages the process and recommends the appointment to the members.

- The members approve the appointment, and the Governance and Nominating Committee chair notifies the successful candidate.

- The director is appointed to the board.

Process for Governor-in-Council appointees

- The selection process is open to all Canadians.

- The Minister of Innovation, Science and Industry, supported by Innovation, Science and Economic Development Canada, manages the process and recommends the appointment to the Governor in Council.

- The Privy Council Office ensures that the proposed appointment meets all requirements.

- The Governor in Council makes the appointment, and the minister notifies the successful candidate.

- The director is appointed to the board.

6.6 The board exercises the foundation’s powers. For example, it

- establishes frameworks for governance and oversight through the Governance and Nominating Committee

- provides strategic direction and establishes key performance indicators through the Human Resources Committee

- hires and appoints the CEO through the Human Resources Committee

- approves projects for funding on the basis of recommendations from the Project Review Committee and approves significant project modifications

- reviews and recommends operating and capital budgets through the Audit Committee

6.7 In addition to having a board, the foundation has members representing people, businesses, and not‑for‑profit organizations that are engaged in the development of technologies that promote sustainable development. According to its enabling legislation, the foundation shall have 15 members. The foundation’s first 7 members were appointed by the Governor in Council, and these 7 members were responsible for appointing 8 further members. Members have the responsibility of appointing 8 of 15 board directors (those not appointed by the Governor in Council), the external auditor of the foundation, and successor members when there are vacancies.

6.8 Innovation, Science and Economic Development Canada. The department is responsible for designing and managing the contribution agreements with the foundation, for monitoring compliance, and for ensuring that the agreements remain relevant to and effective in meeting departmental results and government objectives.

6.9 Since 2015, the foundation has been under the responsibility of the Minister of Industry, now the Minister of Innovation, Science and Industry.

6.10 Parliament authorizes the department’s funding annually. This allows the department to make transfer payments to the foundation in accordance with signed contribution agreements (Exhibit 6.1). Since the foundation’s inception, there have been 9 contribution agreements committing $2.1 billion in funding. The successive contribution agreements also define the criteria for which funding can be distributed by the foundation to finance a project, and these criteria have not significantly changed since 2001.

6.11 The foundation has the authority to award funding and make specific payments to ultimate recipients. At the time of the transfer payment to the foundation, the department does not know whether funds will be spent on eligible projects. The department has rights within the contribution agreements that enable it to oversee public funds and help mitigate risks related to advance payments.

6.12 Objective. The objective was to determine whether between 1 March 2017 and 31 December 2023

- the foundation managed public funds in accordance with the terms and conditions of the contribution agreements and with its legislative mandate

- the department’s oversight ensured that the administration of public funds was in accordance with the terms and conditions of the contribution agreements and with relevant government policies

6.13 Why it matters. This audit is important because the foundation operates at arm’s length from the Government of Canada. To ensure public money is spent in the manner intended, the department must monitor the foundation and ensure that it awarded funding in accordance with contribution agreements.

Findings and Recommendations

Sustainable Development Technology Canada did not establish clear assessment guidance to determine eligibility of projects

6.14 We found that Sustainable Development Technology Canada did not always manage public funds in accordance with the terms and conditions of the contribution agreements for the Sustainable Development Technology Fund. The foundation had not set clear guidance to determine whether projects met all eligibility criteria, and we found that the foundation awarded funding to projects that were ineligible.

6.15 This finding matters because when the foundation awards funding to projects, it must ensure that each project meets the goal and objectives of the Sustainable Development Technology Fund as well as the eligibility criteria of the contribution agreements.

6.16 From 1 March 2017 to 31 December 2023, the foundation approved $856 million of funding to 420 projects through 3 successive contribution agreements for the Sustainable Development Technology Fund. The foundation disbursed funds at agreed‑on milestones when ultimate recipients—the applicants who ultimately received funding—demonstrated they incurred expenses and made progress toward achieving project objectives.

6.17 Before 2019, the foundation had focused on funding clean technology start‑ups, a specific segment of the industry. After receiving an increase in its contributions, the foundation expanded its scope to fund 3 additional segments. The foundation called the segments it invests in “streams.” The streams that existed at the end of our audit period were as follows:

- Start‑up—Funding for companies with a pre‑commercial technology that has been proven at a small scale and that is ready to be validated in a market setting.

- Scale‑up—Funding for advanced, high‑growth companies for pre‑commercial technology projects to accelerate the companies’ growth, strengthen their competitive advantage, or unlock a larger customer base.

- Ecosystem—Funding to develop partners and networks.

- Seed—One‑time funding to support early-stage innovators. Since applicants must be nominated by one of the foundation’s accelerator partner organizations, the funding process for this stream is different from the process shown in Exhibit 6.1.

6.18 The application and approval process for the Start‑up, Scale‑up, and Ecosystem streams over our audit period is shown in Exhibit 6.3:

- Organizations apply for funding through a portal on the foundation’s website.

- The foundation’s staff review and assess applications. They can obtain advice and recommendations from external expert reviewers on business and technical elements for project proposals.

- Management then either rejects the application or recommends the project to the Project Review Committee. The contribution agreements require the committee to screen and assess each recommended project.

- If the committee assessed that the project met the terms and conditions in contribution agreements, it recommends the project to the entire board of directors, who vote to approve or reject the funding for each project.

- Once a project is approved, the foundation enters into a project funding agreement with applicants who become the ultimate funding recipients. The project funding agreement outlines requirements for initial payments and milestones that the ultimate recipients must meet to receive subsequent payments.

Over our audit period, the board approved 226 projects to receive $836 million through these 3 streams.

Exhibit 6.3—Results of applications to the Start‑up, Scale‑up, and Ecosystem streams of Sustainable Development Technology Canada (the foundation), 1 March 2017 to 31 December 2023

Source: Based on Sustainable Development Technology Canada’s project database

Exhibit 6.3—text version

This diagram shows the results of the applications to 3 streams of the foundation Sustainable Development Technology Canada for the period from 1 March 2017 to 31 December 2023.

During the period, there were 532 projects that applied for funding and submitted detailed proposals. Sustainable Development Technology Canada also received 804 applications during the audit period that did not submit a detailed proposal.

Of the 532 detailed proposals that were submitted, 150 were rejected by the foundation.

The remaining 382 detailed proposals that were submitted were reviewed and assessed by the foundation.

Of the 382 detailed proposals that were reviewed and assessed, 134 were rejected by the foundation.

The remaining 248 detailed proposals that were reviewed and assessed were assessed and screened by the board’s Project Review Committee.

Of the 248 detailed proposals that were assessed and screened, 22 were rejected by the board.

The remaining 226 detailed proposals that were assessed and screened were approved by the board. There was $836.2 million approved.

The 226 detailed proposals that were approved by the board can be broken down as follows:

- There were 51 projects completed by ultimate funding recipients. There was $164.3 million approved and $188.2 million spent. Amounts spent can exceed amounts originally awarded when the board and foundation agree to project modifications.

- There were 138 projects ongoing by ultimate funding recipients. There was $517.9 million approved and $326.3 million spent.

- There were 37 projects cancelled or terminated by the foundation. There was $154.0 million approved and $35.2 million spent ($6.2 million considered a debt to the Crown).

6.19 The foundation set up a different process for the Seed stream. Applicants cannot apply directly on the foundation website, but rather must be nominated by accelerator partner organizations. The foundation staff review the application before inviting the applicant in front of a jury panel—made up of non‑foundation clean technology industry executives and sometimes a director from the foundation’s board. Once the panel screens in a Seed project, the funding request is brought to the Project Review Committee and the board for approval. Over our audit period, the board approved 194 projects to receive $19.5 million through this stream.

6.20 After the initial approval of projects, applicants can request project modifications. The foundation’s practice was for the board to approve any projects that had significant scope changes or where the project costs were planned to increase by more than $300,000. The foundation also provided coronavirus disease (COVID‑19) relief payments to ultimate recipients, and these payments were approved as project modifications.

The foundation had not established targets or clear guidance for assessing eligibility criteria

6.21 We examined the 16 projects that were identified in the allegations received by Innovation, Science and Economic Development Canada and a representative sample of 42 additional projects across the Start‑up, Scale‑up, and Ecosystem streams. In all, we reviewed 58 projects. We found that Sustainable Development Technology Canada had not set clear guidance to support staff and the Project Review Committee to determine whether a project met all the eligibility criteria set in the contribution agreements. This lack of clear guidance is important because many criteria required judgment to assess. Furthermore, it was not clear whether any criteria held a greater weight than others.

6.22 To supplement the screening and assessment of project proposals, the foundation engaged 2 external expert reviewers to advise on a project’s technical and business elements and offer recommendations. However, we found that the foundation did not provide them with the eligibility criteria of the contribution agreements. As a result, the reviewers risked recommending projects that did not align with eligibility criteria.

6.23 We also found that the foundation’s staff at times disagreed with the advice of external expert reviewers. We found 9 instances where the foundation rejected applications despite external expert reviewers recommending them. The foundation had the discretion to follow or not the expert recommendation. However, we found that the foundation’s staff rejected some projects because of specific risks, but that it put forward for approval other projects with the same risks. This called into question whether the foundation applied the eligibility criteria in a consistent manner.

6.24 The contribution agreements did not establish targets for the environmental benefits of projects but required each project to quantify them and describe the project’s effects on the environment. The contribution agreements also required the board to approve projects with the greatest merit and through which significant broad benefits would accrue to Canadians. We found that environmental benefits were estimated in all 58 project proposals that we reviewed. However, in our view, in 5 of the 58 projects we examined, estimates presented to the Project Review Committee were unreasonably high. As a result, we extended our work to review third-party assessments of environmental benefits once the projects were completed. We found that in 12 out of 18 completed projects in our sample, the projected reduction of greenhouse gas emissions were, on average, half of what was presented at the time the project proposals were assessed.

6.25 Sustainable Development Technology Canada should

- establish clear guidance to determine when a project meets or does not meet the eligibility criteria set out in contribution agreements

- provide external expert reviewers with the information needed to ensure that they recommend projects that align with the foundation’s mandate

- address the eligibility considerations that the external expert reviewers raise or the recommendations they make

The foundation’s response. Agreed.

See Recommendations and Responses at the end of this report for detailed responses.

6.26 Building on a recommendation made in 2017 by the Commissioner of the Environment and Sustainable Development, Sustainable Development Technology Canada should improve its challenge function over projected sustainable development and environmental benefits.

The foundation’s response. Partially agreed.

See Recommendations and Responses at the end of this report for detailed responses.

The foundation awarded funding to ineligible projects

6.27 For the 58 projects described in paragraph 6.21, we reviewed and analyzed the materials that Sustainable Development Technology Canada had used to screen and assess projects for funding. This included budgets, corporate information, risk assessments, external expert reviewers’ reports, and materials and minutes of the related meetings of the Project Review Committee and the board of directors. We found that 2 Ecosystem projects were clearly ineligible, as they did not fund or support the development or demonstration of a new technology. While we did not perform a technological assessment of projects, we also found 7 Start‑up projects and 1 Scale‑up project where, in our view, the foundation’s documents did not demonstrate that eligibility criteria were met. For example, as raised by some external expert reviewers, the projects did not support the development or demonstration of a new technology, or their projected environmental benefits were unreasonable. Overall, these 10 projects were approved for $59 million in funding, of which $51 million was disbursed as at the end of our audit period.

6.28 Furthermore, since 4 of 42 projects in our representative sample were ineligible, we estimated that 1 in 10 of the remaining 168 Start‑up and Scale‑up projects approved during our audit period, or approximately 16 projects, were also ineligible.

6.29 Sustainable Development Technology Canada should reassess projects approved during the audit period to ensure that they met the goal and objectives of the Sustainable Development Technology Fund and all its eligibility criteria.

The foundation’s response. Partially agreed.

See Recommendations and Responses at the end of this report for detailed responses.

The foundation did not inform Innovation, Science and Economic Development Canada of funding that needed to be recovered

6.30 According to the contribution agreements, when an ultimate recipient cannot provide evidence to Sustainable Development Technology Canada that it used funds for eligible project costs, the foundation must inform Innovation, Science and Economic Development Canada, and the department can recover those funds from the foundation or offset those amounts against subsequent contributions to the foundation. To assess whether the ultimate recipients were using the funding for eligible costs, the foundation monitored the achievement of project milestones before advancing additional funding. However, the foundation did not report in its corporate plan about amounts the department could recover, as it was required to do.

6.31 We found that through the foundation’s milestone management, the foundation terminated 37 project funding agreements that had been approved during our audit period. It determined that $6.2 million needed to be recovered from 12 ultimate recipients because they could not demonstrate that funds were used for eligible project costs. The department was entitled to recover these funds from the foundation, whether the foundation recovered them from ultimate recipients or not. In some cases, the foundation requested less funding from the department to factor in the amounts it had recovered. The foundation, however, did not notify department officials in either situation. Furthermore, we found that the department was not aware of, or did not request, information about terminated funding agreements. This would have allowed the department to identify funds that it was entitled to recover from the foundation. The department began requesting this information only in December 2023.

6.32 Sustainable Development Technology Canada should report regularly to Innovation, Science and Economic Development Canada any amounts owed to the Crown and any amounts it has recovered from ultimate recipients.

The foundation’s response. Agreed.

See Recommendations and Responses at the end of this report for detailed responses.

6.33 Innovation, Science and Economic Development Canada should adjust its subsequent contributions to Sustainable Development Technology Canada to offset for any amounts owing to the Crown.

The department’s response. Agreed.

See Recommendations and Responses at the end of this report for detailed responses.

The foundation poorly managed conflicts of interest

6.34 We found that Sustainable Development Technology Canada’s conflict‑of‑interest policies were not followed 88 times for directors and 2 times for consultants. In addition, we found that the foundation’s bylaws were missing requirements that were outlined in its enabling legislation and that its conflict‑of‑interest policy for directors was not fully aligned with this legislation.

6.35 This finding matters because the foundation is entirely funded through public money. With that comes an expectation that it holds the highest standards for ethical practices. Conflicts of interest that are not disclosed or managed call into question the objectivity and impartiality of the foundation and its decisions. Not managing conflicts of interest—whether real, perceived, or potential—increases the risk that an individual’s duty to act in the best interests of the foundation is affected, particularly when making decisions to award funding.

6.36 The foundation’s directors were subject to conflict‑of‑interest requirements under the Canada Foundation for Sustainable Development Technology Act and the Canada Business Corporations Act. In addition, individuals that were appointed by the Governor in Council to the board of directors are subject to the Conflict of Interest Act and rules for public office holders. These requirements include, among others, the importance of timely disclosures, duty to recuse, abstention from voting, prohibition of giving preferential treatment, and prohibition of the use of insider information.

6.37 In 2018, the foundation established a conflict‑of‑interest policy dedicated to the board and the Project Review Committee. It applied equally to all directors and included an expectation that all directors meet the requirements from the Conflict of Interest Act. Before this time, the directors were subject to the foundation’s conflict‑of‑interest policy that also applied to staff, consultants, and external expert reviewers.

6.38 Best practices for managing conflicts of interest—particularly in the context of the stewardship of public money—help ensure that officials perform their functions with objectivity and impartiality. These practices include that

- officials act in a manner that would bear the closest public scrutiny

- officials arrange their private affairs, where possible, to prevent conflicts of interest arising on appointment and thereafter

- officials recuse themselves from discussions or decisions when they have declared a conflict of interest, real or perceived

- organizations report on the results of conflict‑of‑interest processes to those charged with governance and oversight

The foundation’s records showed that the conflict‑of‑interest policies were not followed in 90 cases

6.39 Overall, we found that Sustainable Development Technology Canada did not have an effective system to maintain records over disclosures of conflicts of interest and related mitigating actions. The foundation used only meeting minutes of the board of directors and of the Project Review Committee to serve as the historical record for conflict‑of‑interest declarations and related mitigating actions.

6.40 We found that the foundation relied on individual directors to send conflict‑of‑interest disclosures in advance of meetings to determine who would receive specific project documentation and recuse themselves at related discussions and voting. The foundation did not consider, or follow up on, previous disclosures to make its own assessment of whether a director might be in a position of conflict. Only in 2022 did the foundation create a register of conflicts of interest declared by directors, which was manually updated to include declarations dating back to 2017. However, as at the end of our audit period in December 2023, there were inconsistencies between information in this register and information contained in meeting minutes.

6.41 We examined the records of all meetings of the Project Review Committee and of the board of directors during our audit period—1 March 2017 to 31 December 2023. These records indicated that directors had followed the conflict‑of‑interest policy and declared conflicts of interest and appropriately recused themselves from voting 96 times.

6.42 However, we found 90 cases where, according to the foundation’s own records, its conflict‑of‑interest policies were not followed:

- According to the meeting minutes, the official corporate records, in 25 cases, directors participated in discussions and voted to approve funding to ultimate recipients despite having previously declared conflicts of interest. For about half these situations, directors informed us that either there was an error in the corporate records and they did not have a conflict of interest, or when they did have a conflict, they recused themselves from voting. While directors had the opportunity to correct the board’s meeting minutes prior to their approval at a subsequent meeting, such corrections were not made.

- Directors voted to approve portfolio‑wide COVID‑19 relief payments in 2020 and 2021. During those 2 votes, in 63 cases, directors voted while having previously declared conflicts of interest. For about a third of these situations, directors informed us that they no longer had a conflict of interest at the time of the votes. However, the foundation had not determined whether these declared conflicts of interest still existed at the time of the votes. Directors informed us that they received legal advice that recusals were not required. In our view, recusal was needed so as to meet the requirements in the conflict‑of‑interest policy.

- The foundation did not remove an external expert reviewer from 2 Scale‑up project assessments despite the individual being involved in another project that had applied for funding. The foundation’s conflict‑of‑interest policy that applied to external expert reviewers did not allow this.

6.43 These 90 cases were connected to approval decisions for nearly $76 million in funding (Exhibit 6.4). Of these, we found that 2 projects, approved for $12 million, were ineligible, as noted in paragraph 6.27. For the remaining cases, we did not identify any business or technical reasons that made these projects ineligible. It is, however, not possible to determine whether outcomes would have been different had directors recused themselves from voting, as the policy required.

Exhibit 6.4—Records showed that conflict‑of‑interest policies were not followed when nearly $76 million of funding was approved during our audit period

| Type of funding | Cases | Funding approved |

|---|---|---|

| Seed stream | 12 | $1.2 million |

| Ecosystem stream | 1 | $5.0 million |

| Start‑up stream | 10 | $24.8 million |

| Scale‑up stream | 4 | $33.0 million |

| COVID‑19 relief payments | 63 | $11.9 million |

| Total | 90 | $75.9 million |

6.44 Finally, we found that the foundation’s conflict‑of‑interest policies lacked specific guidance to address situations that could involve perceived conflicts of interest. It did not establish how to maintain records of decisions about those situations and any potential mitigation strategies. Here are 4 examples:

- In 5 cases, directors had business or personal relationships that we considered gave the appearance that their private interests conflicted with their role of acting in the best interest of the foundation.

- A perceived conflict of interest declared in 2022 by the then‑CEO was not disclosed to the chair of the board, as required by the conflict‑of‑interest policy. Instead, the disclosure was made to the Project Review Committee, which decided that no conflict existed but did not record this decision in the minutes nor its justification. Despite this, months later, the then‑CEO added the conflict to the foundation’s staff-level register, raising doubt as to whether a conflict had existed and, if so, whether it was properly managed.

- The spouse of one of the foundation’s senior managers was a partner at the human resources recruiting firm that the foundation used to support its process to appoint directors, as described in Exhibit 6.2. Since the situation did not involve funding, the foundation’s policy did not establish how potential conflicts should be communicated. The senior manager declared the perceived conflict to the then‑CEO. The board was only made aware of the perceived conflict over a year later, despite this situation relating to board appointments.

- Soon after the board received allegations about financial mismanagement and poor human resources practices at the foundation in January 2023, a special committee of the board was struck. The special committee hand‑selected the same law firm to which the foundation’s external general counsel belonged to investigate and produce a report that the board received in May 2023. This could create the appearance that the investigation was not independent.

6.45 Sustainable Development Technology Canada should implement an effective system to receive, manage, store, and report annually disclosures of conflicts of interest and put measures in place to ensure its conflict‑of‑interest policies are followed.

The foundation’s response. Agreed.

See Recommendations and Responses at the end of this report for detailed responses.

The foundation’s conflict‑of‑interest policies were not aligned with all elements in its legislation

6.46 We found that Sustainable Development Technology Canada’s conflict‑of‑interest policy for directors did not align with certain provisions in its enabling legislation. Subsection 12(2) of the Canada Foundation for Sustainable Development Technology Act states that no director shall profit or gain any income or acquire any property from the foundation or its activities, with an exception for the remuneration received by the foundation’s directors and related expenses. However, the conflict‑of‑interest policy approved by the board only provided for a blackout period that restricted directors from buying or selling securities of companies that applied for funding from the foundation. The blackout period started when a director first received information about a project and ended 3 business days following a public announcement of approved funding.

6.47 In our view, for the duration of a director’s term, a director buying or selling securities of an ultimate recipient—or being compensated by, or holding an investment in, an ultimate recipient receiving funding—risks not following subsection 12(2) of the act. During our audit period, we found 1 case where a director was compensated for consulting fees by an ultimate recipient while its project was still receiving funding. The foundation’s records also showed that directors were invested in 7 companies receiving the foundation’s funding.

6.48 Furthermore, we found an important difference between the rules that applied to the board and those that applied to the foundation’s employees. Notably, the foundation’s rules for employees prevented them from investing in a company funded by the foundation during the term of a project and for a period of 5 years following the project’s completion.

6.49 We also found that the foundation’s bylaws did not include certain provisions required by the Canada Foundation for Sustainable Development Technology Act. The foundation’s bylaws did not include procedures allowing applicants for funding to request that the foundation’s board investigate and make a ruling about a possible conflict of interest of a director on the board.

6.50 Finally, we assessed the foundation’s conflict‑of‑interest policies against best practices and found the following:

- Existing policies did not include a requirement for the foundation’s management to report to the board about its ethical practices.

- The foundation did not inform the Project Review Committee about how staff-level conflicts of interest related to proposed projects were managed. In our view, it is relevant for the committee to consider whether such conflicts were managed before relying on staff assessments to make a recommendation for funding.

- Existing policies did not prescribe how the foundation needed to keep records in situations where decisions over conflict of interest were made verbally. With no record, it becomes difficult for the foundation to put in place mitigation and compliance measures.

- In practice, external expert reviewers were asked to declare any conflicts of interest only for projects to which they were assigned to review. They were not asked about any involvement with the foundation’s other projects, which was information the foundation needed to validate before adding them to the roster of external reviewers.

6.51 Sustainable Development Technology Canada should update its bylaws and its conflict‑of‑interest policies for directors and members to fully align with the Canada Foundation for Sustainable Development Technology Act and best practices in the area.

The foundation’s response. Agreed.

See Recommendations and Responses at the end of this report for detailed responses.

The foundation did not report conflicts of interest to the department

6.52 Since 2018, contribution agreements required Sustainable Development Technology Canada management to report all actual and potential conflicts of interest without delay to Innovation, Science and Economic Development Canada. We found that the department knew of 96 cases when directors declared conflicts of interest because it had access to the meeting minutes and materials of the board of directors. The department was also aware that the approval of COVID‑19 relief payments did not involve any recusals. However, the foundation did not report to the department on

- 91 conflicts of interest that the foundation’s staff had declared

- the 4 situations noted in paragraph 6.44

- the possibility that the foundation’s conflict‑of‑interest policies were not being followed

6.53 In addition to not receiving any reports, we also found that the department had not asked the foundation whether other conflicts of interest existed, or how the foundation was managing conflicts of interest, including whether there had been breaches to any of its codes, policies, or bylaws.

6.54 Sustainable Development Technology Canada should report to Innovation, Science and Economic Development Canada without delay about conflicts of interest, as required by contribution agreements.

The foundation’s response. Agreed.

See Recommendations and Responses at the end of this report for detailed responses.

6.55 Sustainable Development Technology Canada should report to the board of directors about the results of conflict‑of‑interest processes at the organizational level and should disclose project-specific conflicts of interest to the Project Review Committee.

The foundation’s response. Agreed.

See Recommendations and Responses at the end of this report for detailed responses.

The board of directors failed to oversee the foundation’s compliance with key legal requirements

6.56 We found that the board of directors did not oversee Sustainable Development Technology Canada’s compliance with its enabling legislation. Also, in some cases, the board did not follow the process required by the contribution agreements to approve funding.

6.57 This finding matters because the foundation’s board is responsible for overseeing the activities of the foundation, including ensuring that it complies with laws, regulations, and agreements.

Legal requirements for the number of the foundation’s members were not met

6.58 The Canada Foundation for Sustainable Development Technology Act required Sustainable Development Technology Canada to have 15 members. At the start of the audit period, 1 March 2017, the foundation had 14 members. We found that in 2019, the board supported the members’ decision to allow member vacancies to remain unfilled. Despite the fact that Innovation, Science and Economic Development Canada and the board agreed that legislative changes would be required to reduce the number of its members, by 2020, there were only 2 members left and the foundation’s enabling legislation remained unchanged.

6.59 We found that despite there being only 2 members since 2020, these members took the decision to appoint 5 directors to the board of directors and to appoint 1 successor member. The members made these decisions without having the minimum of 5 members to reach a quorum, as required by the foundation’s terms of reference for the members and the foundation’s bylaws. As a result, the board did not ensure that the foundation complied with its enabling legislation.

6.60 Finally, we found that the foundation’s external general counsel also served as a member of the foundation, 1 of only 2 members at the time, who appointed directors to the foundation’s board. In our view, this situation could create a perceived conflict of interest if legal advice was provided to the board that pertained to the foundation’s compliance with its enabling legislation relating to the number of the foundation’s members.

6.61 Sustainable Development Technology Canada should support the foundation’s members to fill required vacancies and ensure that member appointments comply with the requirements in the Canada Foundation for Sustainable Development Technology Act.

The foundation’s response. Agreed.

See Recommendations and Responses at the end of this report for detailed responses.

The board of directors did not consistently follow the terms of contribution agreements or its established practices when it approved funding

6.62 Starting in 2019, Sustainable Development Technology Canada’s management proposed new streams to award funding from the Sustainable Development Technology Fund, as presented in paragraph 6.17. However, we found that the board of directors had not received reports related to the compliance of these new streams with the contribution agreements with the Government of Canada.

6.63 We found that the management team of the foundation had analyzed whether the proposed design of the Seed stream complied with contribution agreements and noted some risks of non‑compliance. Furthermore, we found that Innovation, Science and Economic Development Canada had communicated concerns to the foundation’s management about whether the first Ecosystem project complied with contribution agreements. In both cases, the foundation management did not share these risks or concerns with the board.

6.64 As a result, we found that the board approved $58 million for projects without ensuring that they met the terms of the contribution agreements:

- All the funding the foundation awarded to Seed projects ($19.5 million) was done without the Project Review Committee having the necessary information to screen and assess the projects. For 12 of these projects, we found that the conflict‑of‑interest policy for directors was not followed (see Exhibit 6.4).

- In addition, the 2 COVID‑19 relief payments the foundation awarded (totalling $38.5 million through 220 project modifications) were approved by the board without project-specific analysis to assess the merit of the payment per project. For the COVID‑19 relief payments, we found that the conflict‑of‑interest policy for directors was not followed in 63 cases (see Exhibit 6.4).

6.65 Sustainable Development Technology Canada should adjust its processes to award funding to comply with the requirements in the contribution agreements and in the foundation’s enabling legislation.

The foundation’s response. Agreed.

See Recommendations and Responses at the end of this report for detailed responses.

6.66 To ensure effective oversight by the board of directors, Sustainable Development Technology Canada’s management should report to the board about the foundation’s compliance with applicable laws, regulations, and agreements and should inform the board about any risks of non‑compliance with contribution agreements.

The foundation’s response. Agreed.

See Recommendations and Responses at the end of this report for detailed responses.

The department did not sufficiently assess whether the foundation complied with the contribution agreements

6.67 We found that Innovation, Science and Economic Development Canada did not sufficiently assess and monitor Sustainable Development Technology Canada’s processes to award funding. We also found that the department did not monitor conflicts of interest at the foundation.

6.68 This finding matters because the department is required by government policies to monitor the use of public funds by the foundation.

6.69 The contribution agreements, the Financial Administration Act, the Treasury Board’s Policy on Transfer Payments, the Treasury Board’s Directive on Transfer Payments, and the Treasury Board’s Policy on Results set out several actions that the department can undertake to exercise its oversight of the foundation. These include the following examples:

- Undertake periodic audits and other monitoring activities to ensure that the foundation complied with the contribution agreement.

- Review the foundation’s financial forecasts, corporate plan, and annual report.

- Review internal audit reports of the foundation.

- Review the foundation’s required conflict‑of‑interest disclosures, and make any necessary inquiries regarding conflict‑of‑interest situations.

The department did not sufficiently assess and monitor the foundation and its use of public funds

6.70 We found that Innovation, Science and Economic Development Canada reviewed Sustainable Development Technology Canada’s corporate plans and annual reports, provided input on the foundation’s performance management strategy, and carried out evaluations every 5 years. However, these activities did not provide the department with sufficient information to assess compliance with key requirements of the contribution agreements, such as how projects were screened, assessed, and approved.

6.71 We found that a department employee raised concerns about whether the first Ecosystem project complied with the contribution agreements. However, the department did not take any subsequent actions to address the concerns—for example, by performing an audit to determine whether the foundation had met its contractual obligations or consulting with the department’s legal counsel. Without these actions, the department was not able to assess whether the foundation had complied with all terms and conditions in the contribution agreements. Furthermore, the department supported the foundation’s decision to award COVID‑19 relief payments without ensuring that its process to award such payments complied with contribution agreements.

6.72 We found that the department’s monitoring was insufficient to address risks of non‑compliance with the contribution agreements:

- The department relied on the meeting minutes and materials of the foundation’s board of directors to be informed of the foundation’s operations, use of public funds, or conflict‑of‑interest disclosures. We found that these materials had gaps and did not include all conflicts of interest at the foundation.

- Before each payment to the foundation, a department official assessed the foundation’s cash flow forecast. By design, this assessment could not confirm whether the transfer payments were ultimately spent in accordance with the contribution agreements.

6.73 We found that through these limited actions, the department could not assess whether the foundation complied with the terms of the contribution agreements, despite the requirements of the Treasury Board’s Directive on Transfer Payments. During our audit period, the department did not undertake an audit to determine whether the foundation had met its contractual obligations. Also, it did not request information about audits of ultimate recipients of funding undertaken by the foundation until January 2023.

6.74 An assistant deputy minister of the department regularly attended meetings of the foundation’s board and received all board materials. But neither the department nor the foundation documented what they expected from this role. We found that the directors’ understanding of the assistant deputy minister’s role did not align with his own. This ambiguity led the board to believe that the assistant deputy minister’s presence at meetings provided an implicit agreement by the department for any decisions that the board made.

6.75 Innovation, Science and Economic Development Canada should regularly monitor and audit Sustainable Development Technology Canada to assess whether the foundation complied with contribution agreements.

The department’s response. Agreed.

See Recommendations and Responses at the end of this report for detailed responses.

6.76 Innovation, Science and Economic Development Canada should clarify the role of the department official attending meetings of Sustainable Development Technology Canada’s board of directors and should communicate this to the foundation.

The department’s response. Agreed.

See Recommendations and Responses at the end of this report for detailed responses.

The department did not monitor conflicts of interest at the foundation

6.77 We found that Innovation, Science and Economic Development Canada had not received records of conflicts of interest at Sustainable Development Technology Canada other than those documented in the materials and meeting minutes of the board of directors. Since 2018, the contribution agreements required the foundation to report without delay to the department about conflicts of interest. We found that the department had not asked for or received such information and did not determine what actions it should take when informed of conflicts of interest by the foundation.

6.78 As described in paragraph 6.52, we found several situations that may have involved conflicts of interest that the foundation did not report to the department over the audit period.

6.79 Innovation, Science and Economic Development Canada should ensure that it assesses, challenges, and monitors conflict of interest at Sustainable Development Technology Canada.

The department’s response. Agreed.

See Recommendations and Responses at the end of this report for detailed responses.

Conclusion

6.80 We concluded that

- Sustainable Development Technology Canada did not always manage public funds in accordance with the terms and conditions of the contribution agreements and with its legislative mandate

- Innovation, Science and Economic Development Canada’s oversight did not ensure that the administration of public funds was in accordance with the terms and conditions of the contribution agreements and with relevant government policies

About the Audit

This independent assurance report was prepared by the Office of the Auditor General of Canada on Sustainable Development Technology Canada and Innovation, Science and Economic Development Canada. Our responsibility was to provide objective information, advice, and assurance to assist Parliament in its scrutiny of the government’s management of resources and programs and to conclude on whether the foundation and the department complied in all significant respects with the applicable criteria.

All work in this audit was performed to a reasonable level of assurance in accordance with the Canadian Standard on Assurance Engagements (CSAE) 3001—Direct Engagements, set out by the Chartered Professional Accountants of Canada (CPA Canada) in the CPA Canada Handbook—Assurance.

The Office of the Auditor General of Canada applies the Canadian Standard on Quality Management 1—Quality Management for Firms That Perform Audits or Reviews of Financial Statements, or Other Assurance or Related Services Engagements. This standard requires our office to design, implement, and operate a system of quality management, including policies or procedures regarding compliance with ethical requirements, professional standards, and applicable legal and regulatory requirements.

In conducting the audit work, we complied with the independence and other ethical requirements of the relevant rules of professional conduct applicable to the practice of public accounting in Canada, which are founded on fundamental principles of integrity, objectivity, professional competence and due care, confidentiality, and professional behaviour.

In accordance with our regular audit process, we obtained the following from entity management:

- confirmation of management’s responsibility for the subject under audit

- acknowledgement of the suitability of the criteria used in the audit

- confirmation that all known information that has been requested, or that could affect the findings or audit conclusion, has been provided

- confirmation that the audit report is factually accurate

Audit objective

The objective of this audit was to determine whether

- Sustainable Development Technology Canada (Canada Foundation for Sustainable Development Technology) managed public funds in accordance with the terms and conditions of the contribution agreements and with its legislative mandate

- Innovation, Science and Economic Development Canada oversight ensured that the administration of public funds was in accordance with the terms and conditions of the contribution agreements and with relevant government policies

Scope and approach

This audit examined the management of public funds by Sustainable Development Technology Canada, its actions further to the contribution agreements, and activities carried out by Innovation, Science and Economic Development Canada to oversee the contribution agreements.

We reviewed contribution agreements 7, 8, and 9 for the Sustainable Development Technology Fund. We assessed the design and implementation of controls for the awarding of funding to ultimate recipients on the basis of the relevant clauses, including selection and eligibility criteria. To assess whether the requirements of the contribution agreements were designed and implemented correctly in the foundation’s processes, we conducted interviews with the foundation’s management, external general counsel, directors, and members. We also reviewed documents, including policies and procedures, and analyzed the foundation’s data. We extracted all project-related data from the foundation’s system of records for our audit period. From this population, we examined all relevant documents related to

- the design and implementation of all 16 projects (valued at $109,940,228) that were shared with the department as part of the allegations that were raised

- the design and implementation of a representative sample of 42 out of 210 ($161,980,851 out of the $726,263,615 total approved) projects that were approved by the board of directors through the foundation’s Start‑up, Scale‑up, and Ecosystem streams

- the design of the Seed funding and of COVID‑19 relief payments; however, their implementation was not examined

Where representative sampling was used, samples were sufficient in size to conclude on the sampled population with a confidence level of no less than 90% and a margin of error (confidence interval) of no greater than +10%.

We did not examine the outcomes of the projects that were funded by the foundation.

Criteria

We used the following criteria to conclude against our audit objective:

| Criteria | Sources |

|---|---|

| Sustainable Development Technology Canada manages public funds in accordance with contribution agreements. |

|

| The board of directors and council members carry out oversight of Sustainable Development Technology Canada in accordance with its legislative mandate and applicable terms and conditions in the contribution agreements. |

|

| Sustainable Development Technology Canada’s processes for managing conflicts of interest meet the requirements in applicable legislation, codes, and contribution agreements and are consistent with best practices. |

|

| Innovation, Science and Economic Development Canada, in alignment with the applicable powers and obligations, exercises oversight of Sustainable Development Technology Canada and its use of public funds. |

|

Period covered by the audit

The audit covered the period from 1 March 2017 to 31 December 2023. This is the period to which the audit conclusion applies. However, to gain a more complete understanding of the subject matter of the audit, we also examined certain matters that preceded the start date of this period.

Date of the report

We obtained sufficient and appropriate audit evidence on which to base our conclusion on 29 May 2024, in Ottawa, Canada.

Audit team

This audit was completed by a multidisciplinary team from across the Office of the Auditor General of Canada led by Mathieu Lequain, Principal. The principal has overall responsibility for audit quality, including conducting the audit in accordance with professional standards, applicable legal and regulatory requirements, and the office’s policies and system of quality management.

Recommendations and Responses

Responses appear as they were received by the Office of the Auditor General of Canada.

In the following table, the paragraph number preceding the recommendation indicates the location of the recommendation in the report.

| Recommendation | Response |

|---|---|

|

6.25 Sustainable Development Technology Canada should

|

Sustainable Development Technology Canada’s response. Agreed. Each project proposal goes through rigorous due diligence and evaluation against the eligibility criteria including but not limited to what is set out in the contribution agreement (CA). This robust due diligence is highly credible and valued by public and private sector investors, resulting in every dollar invested by the foundation unlocking $7 in follow‑on financing. Proposals are subject to approximately 200 hours of due diligence by highly trained and experienced staff, and 36 hours by at least two external expert reviewers who are provided assessment templates with eligibility criteria from the CA. Expert reviewer feedback is always considered and incorporated into final assessments. During the audit period, 94% of the applications recommended by external reviewers moved forward to the Project Review Committee. The Project Review Committee, comprised of individuals with expertise related to technologies that promote sustainable development, thoroughly reviews all materials and engages in robust discussions on the eligibility and merits of projects. In November 2023, Sustainable Development Technology Canada strengthened the documentation of its approvals processes, including establishing clear guidance on project eligibility assessment against criteria in the CA and updated guidance and training materials for external reviewers. Sustainable Development Technology Canada will explore additional opportunities for improvement. |

|

6.26 Building on a recommendation made in 2017 by the Commissioner of the Environment and Sustainable Development, Sustainable Development Technology Canada should improve its challenge function over projected sustainable development and environmental benefits. |

Sustainable Development Technology Canada’s response. Partially agreed. Sustainable Development Technology Canada (SDTC) employs a robust process to quantify projected potential environmental benefits across 12 impact areas, at three different points during a project lifecycle. The process follows recognized standards. A 2018 Innovation, Science and Economic Development Canada evaluation found that SDTC had a substantial review and challenge process for assessing proposed environmental benefits in project proposals. During due diligence, the best information available is used to quantify environmental impacts and is thoroughly reviewed and challenged by SDTC staff trained in environmental benefits quantification. After approval, SDTC uses external experts to quantify benefits and refine estimates two additional times as the project progresses. Inherent uncertainties exist in projecting the environmental benefits of novel pre‑commercial technologies. Information is often limited and involves estimating impacts 10‑15 years into the future. Substantial increases or decreases in estimated benefits are expected as the technology gets closer to commercialization. In 2021, the foundation engaged a third-party expert in sustainable benefits quantification to support the benchmarking of SDTC’s processes and implemented a methodology for more effectively comparing the projected benefits across projects and to inform funding decisions. SDTC will continue to improve its challenge function regarding projected sustainable development and environmental benefits. |

|

6.29 Sustainable Development Technology Canada should reassess projects approved during the audit period to ensure that they met the goal and objectives of the Sustainable Development Technology Fund and all its eligibility criteria. |

Sustainable Development Technology Canada’s response. Partially agreed. The Fund’s objectives are to contribute to Canada’s environmental objectives and sustainable economic growth, and enable Canadian companies to compete globally. Sustainable Development Technology Canada (SDTC) has delivered strong outcomes against these objectives. For example:

SDTC acknowledges that findings relating to Start‑up/Scale‑up project eligibility were based on the documents considered by the Office of the Auditor General of Canada (OAG). In our view, these written records did not fully capture the robust deliberations made by the Project Review Committee, which were informed by in‑depth due diligence (see #25) and by their collective judgement stemming from deep expertise in the sector. SDTC is of the view that these projects met the eligibility criteria set out in the contribution agreement but acknowledges that the OAG reached a different conclusion given that this additional perspective was not fully captured in the scope of the written information available to the OAG. In cooperation with Innovation, Science and Economic Development Canada, SDTC will reconfirm that active projects meet the goal, objectives and eligibility criteria set out in the contribution agreement. |

|

6.32 Sustainable Development Technology Canada should report regularly to Innovation, Science and Economic Development Canada any amounts owed to the Crown and any amounts it has recovered from ultimate recipients. |

Sustainable Development Technology Canada’s response. Agreed. All recoveries by Sustainable Development Technology Canada (SDTC) are offset against future transfer payments from Innovation, Science and Economic Development Canada (ISED), as allowed in the contribution agreement. The foundation has strong monitoring processes in place to ensure that payments to all approved projects comply with the criteria for eligible project costs in the contribution agreements. SDTC sequences the disbursement of funds according to a milestone schedule and has rigorous processes in place to monitor a project’s progress prior to advancing funding. This includes assessments of project scope, schedule performance against objectives, eligibility of costs and financial capacity to complete the project. The disbursement process is supported by project financial audits led by external audit firms. The project monitoring processes ensure all disbursed funding is accounted for and mitigates the risk of the non‑recovery of funds. SDTC strengthened the documentation of its recovery of funds processes as part of the management response action plan submitted to ISED in November 2023, which was reviewed by a third party to ensure best practices were incorporated. SDTC will submit quarterly reports to ISED, outlining amounts owed for projects where funding did not meet the terms and conditions of agreements and will report all amounts owing to the Crown in its corporate plan. |

|

6.33 Innovation, Science and Economic Development Canada should adjust its subsequent contributions to Sustainable Development Technology Canada to offset for any amounts owing to the Crown. |

Innovation, Science and Economic Development Canada’s response. Agreed. The Department will ensure that future contribution payments to the Foundation are adjusted to offset amounts owing to the Crown. To enhance transparency, going forward, the Foundation will be asked to report on a regular basis whether any amounts are owing to the Crown, including in each of its annual corporate plans, and to indicate any such amounts. This will ensure consistent communication to the Department from one corporate plan to the next. |

|

6.45 Sustainable Development Technology Canada should implement an effective system to receive, manage, store, and report annually disclosures of conflicts of interest and put measures in place to ensure its conflict‑of‑interest policies are followed. |

Sustainable Development Technology Canada’s response. Agreed. Sustainable Development Technology Canada (SDTC) had clear processes for staff and directors to declare real, potential and perceived conflicts but agrees that an improved system to manage, store and report conflict declarations and their adjudication was needed. In November 2023, SDTC strengthened its conflict of interest (CoI) policies and processes, including the creation of a more effective system for recording and managing declared CoIs. SDTC updated its Code of Ethics and strengthened training and internal audits to ensure adherence to the Code, CoI policies and processes. These policies and processes were reviewed by a third-party firm to ensure best practices were incorporated. SDTC has also:

SDTC’s internal audit function will review annually adherence to the CoI policy. SDTC notes that if its CoI register had been updated regularly to remove conflicts that no longer existed, and that adjudications of potential conflict had been properly documented, the number of cases noted in Exhibit 6.4 would have reduced by at least 41 cases. |

|

6.51 Sustainable Development Technology Canada should update its bylaws and its conflict‑of‑interest policies for directors and members to fully align with the Canada Foundation for Sustainable Development Technology Act and best practices in the area. |

Sustainable Development Technology Canada’s response. Agreed. Sustainable Development Technology Canada (SDTC) will update its by‑laws to align with the requirements of the Canada Foundation for Sustainable Development Technology Act. Section 11(a) of the Canada Foundation for Sustainable Development Technology Act, which came into force in 2001, states “the need to ensure, as far as possible, that at all times the board will be representative of (i)Persons engaged in the development and demonstration of technologies to promote sustainable development, including technologies to address issues related to climate change, and the quality of air, water and soil” As potential for conflict is inherent in the Act, SDTC further strengthened its conflict‑of‑interest policies. In November 2023, SDTC updated its Code of Ethics and strengthened training materials for all parties subject to the policy. The policies were reviewed by a third-party firm to ensure best practices were incorporated. The policy will be reviewed regularly by SDTC’s Ethics Advisor and will undergo regular internal audits for compliance. The foundation will also improve minuting of disclosures, adjudication of conflicts and recusals at board and committee meetings to ensure that SDTC’s standard practice of directors exiting board and committee meetings when they have a declared conflict of interest is properly and consistently reflected in all official records. |

|

6.54 Sustainable Development Technology Canada should report to Innovation, Science and Economic Development Canada without delay about conflicts of interest, as required by contribution agreements. |

Sustainable Development Technology Canada’s response. Agreed. Sustainable Development Technology Canada (SDTC) has updated the process and frequency of its reporting to Innovation, Science and Economic Development Canada (ISED) on conflict of interest through the management response and action plan submitted to ISED in November 2023. The process was reviewed by a third-party firm and by SDTC’s Ethics Advisor. Going forward, SDTC will provide ISED an updated list of conflict disclosures on a regular basis on an agreed upon timeline. SDTC will continue to work with ISED to align processes for reporting conflicts of interest as required by contribution agreements. |

|

6.55 Sustainable Development Technology Canada should report to the board of directors about the results of conflict‑of‑interest processes at the organizational level and should disclose project-specific conflicts of interest to the Project Review Committee. |

Sustainable Development Technology Canada’s response. Agreed. Sustainable Development Technology Canada (SDTC) staff are required to adhere to a robust code of conduct, conflict of interest and internal trading policies and procedures. SDTC employees declare any real, potential, or perceived conflicts as soon as they become aware of them and redeclare any existing conflicts monthly. As noted in this report, SDTC’s rules prevent employees from investing in a company funded by the foundation until five years following project completion. Staff must also divest any pre‑existing assets or interests in funded companies upon joining SDTC. SDTC has strengthened its existing conflict of interest processes as part of the management response action plan submitted to Innovation, Science and Economic Development Canada in November 2023, which was reviewed by a third-party firm and SDTC’s Ethics Advisor to ensure that best practices are incorporated. Declarations and mitigations plans are now reviewed by SDTC’s Ethics Advisor, who provides recommendations on the management of any conflicts. Through our strengthened processes, SDTC will ensure that the board of directors and Project Review Committee are aware of relevant conflicts at the organizational level. Under the guidance of SDTC’s Ethics Advisor, the foundation will continue to evolve our conflict‑of‑interest processes. |

|

6.61 Sustainable Development Technology Canada should support the foundation’s members to fill required vacancies and ensure that member appointments comply with the requirements in the Canada Foundation for Sustainable Development Technology Act. |

Sustainable Development Technology Canada’s response. Agreed. Sustainable Development Technology Canada will support the foundation’s members to fill required vacancies and comply with the requirements in the Act. A key function of the members is to appoint non‑Governor‑in‑Council appointed directors. The foundation follows a rigorous appointment process, implemented in 2016 following a third-party governance review, and is led by the Governance and Nominating Committee (GNC) of the Board. The GNC maintains a skills matrix of Board members, which identifies gaps that need to be filled when new directors are appointed. The skills matrix is informed by the requirements of the Act. To ensure complete impartiality in the identification of suitable candidates, the GNC retains an external recruitment firm to assist with the search for new directors. The external firm sources a roster of qualified candidates from across Canada and ensures that a structured interview process is in place. Qualified candidates are then interviewed by the GNC. The GNC recommends to the Board the successful candidates. The Board then recommends these to the members. The members undertake a final step in vetting the process and the successful candidates. This process helps ensure that the Sustainable Development Technology Canada Board is diverse, representative of Canada, and has the necessary skills to discharge its duties. |

|

6.65 Sustainable Development Technology Canada should adjust its processes to award funding to comply with the requirements in the contribution agreements and in the foundation’s enabling legislation. |

Sustainable Development Technology Canada’s response. Agreed. Sustainable Development Technology Canada (SDTC) will ensure that its processes to award funding across all funding streams comply with the contribution agreement and enabling legislation. As referred to in Management Responses #25 and #45, SDTC has rigorous due diligence and evaluation processes and has strengthened its conflict‑of‑interest policies and processes. Through the management response action plan submitted to Innovation, Science and Economic Development Canada (ISED) in November 2023, SDTC has further strengthened all business processes related to the award of funding and to ensure compliance with the contribution agreements and enabling legislation. These processes were reviewed by a third-party firm to ensure best practices were incorporated. SDTC is also actively working with ISED to update SDTC’s contribution agreement. In August 2023, SDTC created an internal audit function which reports directly to the Audit Committee of the Board. The function assesses SDTC’s compliance with contribution agreements and its enabling legislation, as well as SDTC’s internal policies, procedures, management and information systems and controls established by the board. The internal audit function will report the results of the audits directly to the Audit Committee. All reporting will also be shared with ISED. |

|

6.66 To ensure effective oversight by the board of directors, Sustainable Development Technology Canada’s management should report to the board about the foundation’s compliance with applicable laws, regulations, and agreements and should inform the board about any risks of non‑compliance with contribution agreements. |

Sustainable Development Technology Canada’s response. Agreed. Sustainable Development Technology Canada (SDTC) employs an Enterprise Risk Management Framework to identify and manage risks at a strategic level. On a semi‑annual basis management and the board identify and review strategic risks and mitigation strategies are put in place. SDTC conducts internal audits to assess compliance with operational policies and procedures, which are then reported to the Audit Committee. To complement this oversight, in August 2023, SDTC created a dedicated internal audit function which conducts regular internal audits to assess SDTC’s compliance with contribution agreements and reports the results of the audits, including any risks of non‑compliance, directly to the Audit Committee. All reporting will be shared with Innovation, Science and Economic Development Canada (ISED). In addition to the internal audit function, SDTC has strengthened its existing due diligence and project monitoring processes ensuring continued compliance to the contribution agreement, as part of the management response action plan submitted to ISED in November 2023. These processes were reviewed by a third-party firm to ensure best practices were incorporated. SDTC is working with ISED on updates to the contribution agreement. These updates include additional provisions to verify compliance to the contribution agreement should any substantial changes be made to funding streams and due diligence processes. |

|

6.75 Innovation, Science and Economic Development Canada should regularly monitor and audit Sustainable Development Technology Canada to assess whether the foundation complied with contribution agreements. |